Image: via cnevpost.com

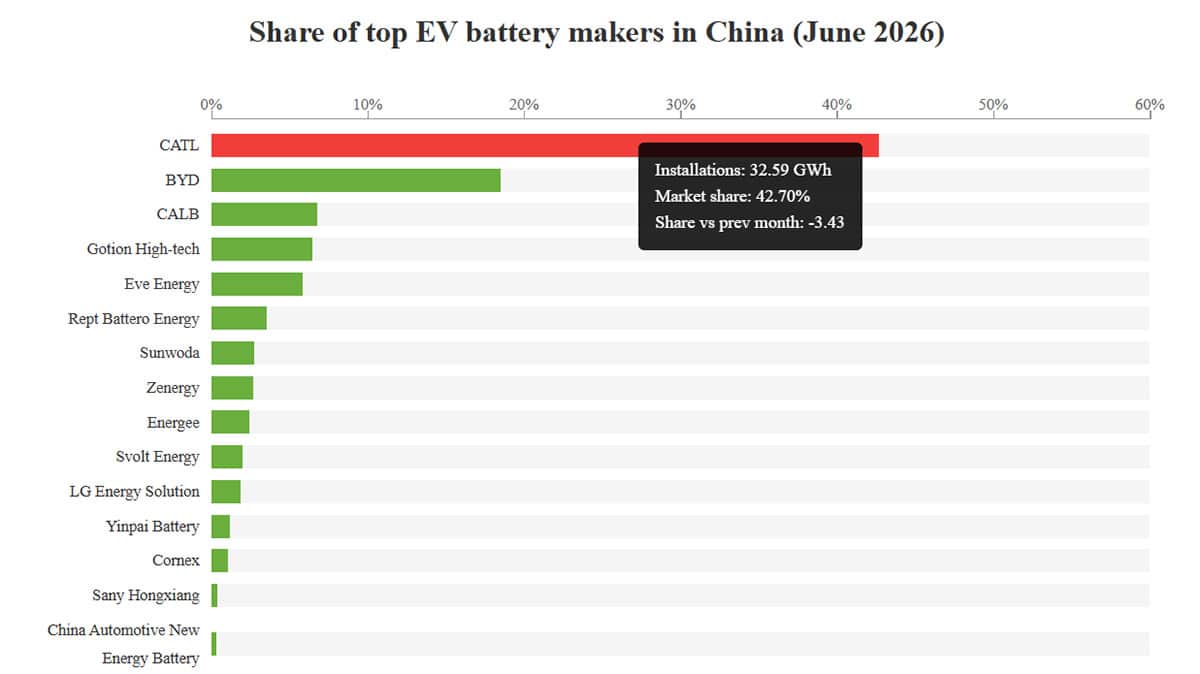

China’s EV battery market stayed highly concentrated in June 2026. CATL remained in front, while BYD posted a clear gain, according to data from the China Automotive Battery Innovation Alliance.

CATL held a 42.70% share with 32.59 GWh of installations. BYD rose to 18.49% with 14.11 GWh. Together, the two controlled 61.19% of the market.

Why this matters for Nepal

For Nepali buyers, this is a China industry update with local ripple effects. Nepal imports a large share of its electric cars through regional supply chains tied to China and India, so the balance between CATL and BYD can affect which battery packs show up in popular EVs sold here, along with cost and range positioning.

CATL’s share fell by 3.43 percentage points from the previous month, even though it stayed far ahead of every rival. BYD’s share increased by 1.92 percentage points. Its month-on-month installations grew nearly 19%.

The battery mix also leaned toward lower-cost chemistries. LFP batteries accounted for 83.3% of China’s total power battery installations in June, a record high, while ternary batteries dropped to 16.5%. That matters for Nepal because LFP-based EVs are often associated with lower battery cost, better cycle life, and competitive pricing in mass-market models.

Among the top five makers, CALB moved to third, Gotion High-tech slipped to fourth, and Eve Energy climbed to fifth. The wider picture is unchanged. China’s battery market is still dominated by a few large suppliers, and that can influence global EV pricing and the features available in imported models sold in Nepal.

For Nepali car shoppers, the immediate effect is likely indirect rather than model-specific. Stronger competition among battery suppliers can support more affordable EVs over time. It can also create variation in range and charging performance, depending on which battery maker a brand chooses for a given vehicle.

Reported by the Nepal AutoMart news desk. Prices verified against Nepal AutoMart's own distributor-sourced data.